Obsidian Memo] Closing the Circle: The Family Legacy Conversation We Are Not Having Enough - Family Office Example

Inheritance and family legacy don't have to carry darkness and dysfunction. A new framework for how families can pass forward wealth, values, and responsibility — with clarity, integrity, and light. Drawing on a conversation with Christina Wing, Harvard Business School professor.

![Obsidian Memo] Closing the Circle: The Family Legacy Conversation We Are Not Having Enough - Family Office Example](https://images.unsplash.com/photo-1564679477577-15a98abb4ee8?crop=entropy&cs=tinysrgb&fit=max&fm=jpg&ixid=M3wxMTc3M3wwfDF8c2VhcmNofDl8fGNpcmNsZXxlbnwwfHx8fDE3NzU5MDI4NjV8MA&ixlib=rb-4.1.0&q=80&w=1200)

Reformed Heritage.

Close this circle so the bloodline can be freed into ease.

Carry the future line as keeper and steward — so that peace may return.

Let the worlds collapse so the future can write itself — in purity.

In abundance. In light. And in integrity. - EJ Elena Shin

Reformiertes Erbe.

Schließe diesen Kreis, damit die Blutlinie in Leichtigkeit befreit werden kann.

Trage die zukünftige Linie als Hüterin und Verwalterin – damit der Frieden zurückkehren kann.

Lass die Welten zusammenfallen, damit die Zukunft sich selbst schreiben kann – in Reinheit.

In Fülle.

In Licht.

Und in Integrität. - EJ Elena Shin

Personal Note

Hi All,

Let me start with something a little lighter before we go deep.

Growing up, I loved Arrested Development. If you know the show, you know the Bluth family — a wealthy, dysfunctional mess of a family where nobody knows where the money actually is, nobody talks about it honestly, and everyone is either gaming the system or completely in the dark about it. The patriarch built an empire and kept every card close to his chest. His children grew into adults who were brilliant in their own chaotic ways but completely unprepared — financially, emotionally, structurally — for any kind of real stewardship. It is comedy gold. It is also, if you look at it straight, a documentary.

Then there is Succession. Less funny. Much darker. The Roy family as a portrait of what happens when inheritance becomes a weapon — when the conversation about succession never really happens, it just becomes a game of power and manipulation that nobody wins. Logan Roy's children spend the entire series auditioning for a role their father never intends to give them. They are smart, ambitious, capable in their own ways — and completely hollowed out by the ambiguity of what they are supposedly inheriting and whether they are even wanted in it.

I bring these up not to be glib. I bring them up because both of these fictional families are everywhere in real life, and because I believe we can do so much better — and I am genuinely excited about the possibility of that.

Enjoy!

I. Why This Topic Does Not Have to Be Dark

When people hear "family office" or "inheritance" or "generational wealth," there is an immediate gravitational pull toward the darker associations. Secrecy. Suspicion. Stories of corruption, manipulation, coercion. The idea of old money operating behind governments and above ordinary rules. People with more power than accountability. Children used as pawns in dynasties.

I understand where that comes from. Some of it is real.

But I refuse to let that be the only story.

What I am passionate about — what genuinely lights me up — is the other possibility. What it looks like when a family decides to do this with integrity. With transparency. With a real mission and real values and real conversations that most families are too afraid to have. The family office or family trust not as a vehicle for concentrating power but as a structure for releasing the bloodline into ease — carrying the future line as keeper and steward, so that peace can return.

That is the vision. That is what Reformiertes Erbe means to me. Reformed heritage. Not rejecting what came before, but consciously, deliberately choosing to carry it forward differently.

This post is for everyone thinking about that — whether you have material wealth to pass on, or whether your inheritance is a name, a set of values, a community, a way of doing things that matters. Legacy is not only about money.

II. The Business Nobody Wants to Call a Business

Here is a truth that Christina Wing, who teaches the family enterprise course at Harvard Business School, puts plainly: roughly ninety percent of family offices are structured incorrectly.

Not because the families are not smart. Not because they do not care. But because they do not treat the family office as what it actually is — a business.

The moment a family creates a formal structure to manage wealth and legacy across generations, it has created a business. And like any business, it needs a clear purpose, a plan, the right people in the right roles, and metrics that actually mean something.

Instead, what often happens is: someone has a liquidity event, or inherits wealth, and they hire their best friend or their cousin because they trust them. Trust is beautiful. Trust is not a job description. And trusting someone with your personal life is genuinely different from trusting them to grow, protect, or deploy generational capital.

The best family offices — the ones that actually hold up over time — go slow to go fast. They ask the question that sounds almost too simple: what is this money actually for?

Is it for preservation? For growth? For giving away? For creating jobs and building businesses? These are not the same answer and they do not lead to the same team, the same structure, or the same definition of success.

Structure matters because it protects people — the family, the employees, and the mission itself. Separating the investment function from the administrative function from the philanthropic function is not bureaucracy for its own sake. It is how you give each person a clear mandate, a clear way to measure their work, and the dignity of knowing what they are actually accountable for. When everything is tangled together, nobody can answer the most basic question: did we do our job?

III. What Getting It Right Actually Looks Like

Christina is careful to say that we are still in early innings — that the family office world is young compared to, say, the multi-generational operating company world, and that even the best examples are still works in progress. But there are families and structures worth learning from, precisely because of the principles they embody rather than the scale of their wealth.

- The Koch family is one of the clearer illustrations of structural clarity done well. Koch Industries is a founder-driven operating business. Separately — and the separation is the point — the Koch family office is its own entity, completely distinct from the company. And within that family office, they have gone one step further: the investment function is based in Denver, staffed like a serious investment firm, paid accordingly, and focused entirely on one thing — growing the money. The concierge and administrative function — estate planning, taxes, lifestyle management — sits in an entirely different state and has an entirely different mandate. And Charles Koch's philanthropic work, Stand Together, is a third separate entity based in DC, with its own team and its own definition of success.

- Three functions. Three mandates. Three locations. Each team knows exactly what it is being measured on. Nobody is trying to simultaneously optimize investment returns and remember to pay the tuition on time. That clarity, Christina argues, is what allows each function to actually push and improve rather than just maintain.

- MSD Capital — the Michael Dell family office — is perhaps the most cited example of a family office that genuinely ran like a top-tier investment firm, because it was structured to be one. Michael Dell gave his CIO, John Failen, a remarkably clear mandate: make money. He separated the investment function from everything else, gave the team autonomy over hiring and compensation, stayed in Texas while the investment team operated in New York, and — crucially — stayed out of the way. The pitch Dell reportedly made was essentially: I will give you permanent capital so you never have to raise money again. I will open doors with my relationships. I will not meddle. And you will get paid like you are running a private equity firm, because that is what you are doing.

- That model worked for over twenty years. That is, as Christina notes, longer than many private equity fund cycles. The lesson is not that you need Michael Dell's resources to replicate it — it is that the clarity of the mandate, the seriousness of the compensation structure, and the founder's genuine willingness to be hands-off were the real ingredients. Those are principles, not price tags.

- The Pritzker family offers yet another model — one where the family office itself became a platform for raising capital from other families, effectively taking the private equity model in-house. Rather than outsourcing fund management and paying fees and carry to external managers, they built investment capability internally, then invited other family offices to co-invest alongside them. Over time, as track record accumulated, that co-investing evolved into formal fund structures. The family office stopped being purely a cost center and started generating its own revenue — management fees and carry from external capital — while giving the internal team the kind of economic participation that keeps elite talent from walking out the door.

- What these three examples share is not size. It is intentionality. A clear answer to the question: what is this structure for, and how will we know if it is working? The families that struggle, Christina observes consistently, are the ones that never answer that question clearly — or answer it differently depending on who is asking and on what day.

IV. The Conversation That Is Not Happening

This is the part of a recent podcast episode with Christina Wing that struck me the most — and that I have not been able to stop thinking about.

In many families, nobody talks about the inheritance. Nobody talks about the succession plan. And the bigger the wealth, the more opaque and last-minute the conversation tends to be.

Which means that so many Gen 2 and Gen 3 and beyond grow up in total darkness about what they are stepping into — or being asked to step into, or being quietly excluded from. They see the private plane. They feel the weight of a name. They sense that something large exists. But nobody will name it, quantify it, or tell them what their role in it might be.

And here is what I want to ask directly: how are you supposed to plan your life with that ambiguity?

How do you make career decisions? Partnership decisions? Decisions about who you want to be, what you want to build, what risks are yours to take — when you genuinely do not know what resources or responsibilities you might one day be holding?

The fear behind this silence is understandable. Parents worry: if I tell my children how much there is, they will stop trying. They will lose hunger. They will become the cautionary tale.

But the evidence does not really support this fear. What the evidence does support is that children raised in this ambiguity either guess — and often guess wrong — or they wait, indefinitely, in a kind of suspended animation that makes it nearly impossible to build a real autonomous life. The silence is not protection. It is, however unintentionally, a form of control.

V. In Defense of Gen 2 and Gen 3

I want to say this clearly because I feel strongly about it and I have seen it with my own eyes.

The stereotype that Gen 2 and Gen 3 are soft, entitled, without grit or drive — I think it is often profoundly unfair and I think it misses what is actually going on.

Gen 1 founders are extraordinary people. They are also, frequently, extremely difficult people. Intense to the point of their own detriment. Flaws in character that got baked in alongside the strength that built the empire. Controlling. Often emotionally unavailable in the specific way that people who have bet everything and won tend to be. Extremely resistant to change. Exhausting to be around and to be raised by.

So when we look at Gen 2 and wonder why they are different — why they do not have the same raw hunger, the same all-in recklessness, the same willingness to blow everything up in service of the vision — I think we owe them some empathy. They grew up in that household. They absorbed all of it. The weight of the legacy, the silence about the money, the impossible standard of a parent who built something from nothing and can never quite let anyone else touch it.

And still — so many of them are hungry. Hungry to create their own story. To not just carry a name but to do something worthy of it. To take what was built and use it to change something real in the world. I have seen this. It is real.

What Christina says: what they need is not lower expectations. What they need is a clear invitation. They need Gen 1 to say — genuinely — our family is built on entrepreneurship. That is the thing you are inheriting. Go build something. The form can change. The spirit cannot.

And they need to be allowed to fail. Not catastrophically. But meaningfully. If every mistake is treated as evidence of unworthiness, the rational response is to stop trying anything that could end in a mistake. You produce caution. You produce risk-aversion. You produce people who look like they have no drive when really they have just learned that drive is dangerous in this family.

Give Gen 2 and Gen 3 the information. Give them the invitation. Give them a safe container for failure and a clear sense of what the mission actually is. Most of them will rise to it.

VI. What It Could Look Like Instead

This is what Christina shared — a template, a framework, a new kind of family office or family trust structure that is built on a completely different foundation. Not secrecy but transparency. Not control but stewardship. Not ambiguity but clarity — about the money, the mission, the roles, the values, the plan.

Some of what this looks like in practice:

- Start with the mission, before anything else: What is this structure actually for? What are the family's values? What does success look like across generations — not just financially but humanly? This question has to be answered before you hire anyone, create any legal entity, or make any investment decisions. You cannot build the right team without a clear mission. You will just build a team.

- Separate what needs to be separate: Investment management, administrative and concierge services, philanthropic strategy — these are three different functions and they thrive under three different kinds of accountability. Keep them clear. Let each have a mandate. Let each be measured honestly.

- Pay people as if their work matters: Because it does. The talent required to steward generational wealth is being recruited every day by private equity, by hedge funds, by venture capital. The pitch that family offices offer — permanent capital, no fundraising treadmill, genuine autonomy, long time horizons — is genuinely compelling. But only if the reality matches the pitch. Pay competitively. Align incentives with mission. Give people a reason to stay and to push.

- Have the conversation about money: With your children, starting earlier than feels comfortable, with increasing depth as they mature. Not as a disclosure event. As a relationship. As an ongoing, honest, evolving conversation about what the family has built, what it values, and what it hopes to pass forward.

- Have the conversation about death: About succession. About what the estate plan says. About who leads what and what happens when the founders are gone. This is love. This is the most responsible thing.

- Treat the rising generation as partners, not heirs on probation: Include them in governance. Let them make decisions. Let them make some mistakes. Define what entrepreneurship means for their context and hold them to the spirit of it — not as a test but as an expression of shared identity.

VII. Closing the Circle

Reformiertes Erbe. Reformed heritage.

Not a rejection of what Gen 1 built. A conscious, deliberate, luminous continuation of it. Carrying the future line as keeper and steward. Letting the worlds converge so the future can write itself — in purity, in abundance, in light, and in integrity.

This is possible. It is not the dominant story yet, but it is being built in pockets by families who are willing to do the hard work of honesty — with each other, with the next generation, with the people they bring onto their teams.

The Bluths make us laugh because the alternative — watching a family get it so spectacularly wrong without the laugh track — is just heartbreak. The Roys make us uncomfortable because we recognize something in them. The inheritance question handled badly, the conversation avoided for too long, the next generation left holding ambiguity where a plan should have been.

You do not have to be either of those families.

The circle can be closed differently. The bloodline can be freed into ease.

That is what I am working toward. I would love to hear if it resonates with you.

This post was inspired by a conversation with Christina Wing, who teaches the family enterprise course at Harvard Business School and advises families through her private practice, Wingspan. Her work on family offices as businesses — and her advocacy for the rising generation — informs much of what is explored here.

Other resource you might want to check out:

*Bonus: The Real Numbers — How Big Are These Family Offices, and Is This Even an American Idea? (AI-generated)

The Three Family Offices in This Post — Scale and Current Status

1) Koch family — 1888 Management / 1888 Investments (Wichita, Kansas / Denver, Colorado — founded 2014)

The Koch family office, formally called 1888 Management LLC (named after the year Koch patriarch Harry Koch immigrated to America), was incorporated in Delaware in 2014 and operates primarily out of the Denver area under CIO Trent May. The AUM of 1888 itself is not publicly disclosed — the last reported figure put it at over $2 billion in directly managed personal investments — but this represents only the personal investment vehicle, not the full Koch complex. Charles Koch's personal net worth stands at approximately $53 billion. The family's broader investment footprint is substantially larger: Koch Real Estate Investments recently became the largest institutional shareholder of Amherst, a platform managing $16.4 billion across single-family rental and commercial real estate. The philanthropic arm, Stand Together, operates separately out of Washington DC as a distinct entity entirely.

The three-part structure — 1888 Investments for personal capital, Koch Real Estate Investments for property, Stand Together for philanthropy — is structurally exactly what Christina Wing describes as best practice: separate mandates, separate teams, separate accountability.

2) MSD Capital / DFO Management — the Michael Dell family office (New York City, with offices in Santa Monica and West Palm Beach — founded 1998)

This is the most structurally evolved of the three examples, and its recent history is worth understanding clearly. MSD Capital was founded in 1998 by Michael Dell to manage his family's wealth. It ran as a single-family office for over two decades, generating more than $17 billion in profits between 1998 and 2019. In December 2022, it was formally restructured and renamed DFO Management, LLC — the pure Dell family vehicle — while its external investment arm, MSD Partners, merged with Byron Trott's merchant bank BDT & Company to form BDT & MSD Partners in January 2023. The combined BDT & MSD platform reported $50 billion in AUM in 2023. MSD Partners alone carried approximately $23.1 billion in AUM as of June 2025.

What began as a model family office has become one of the more significant institutionalised investment platforms in the world. This is itself a lesson: when you build a family office correctly — elite talent, clear mandate, competitive pay, hands-off founder — you may end up with something that outgrows the original structure entirely.

3) The Pritzker family — The Pritzker Organization / Pritzker Group (Chicago and New York — family office history spanning 70+ years)

The Pritzkers are the hardest of the three to pin to a single number, deliberately so. The family has multiple branches, each operating through its own vehicle: The Pritzker Organization (TPO), led by Tom Pritzker; Pritzker Group; Pritzker Private Capital; DNS Capital (Gigi Pritzker's office); and Pritzker Vlock, among others. The Pritzker Organization alone has worked on approximately 300+ transactions representing around $40 billion of equity value over its 70-year history. Total Pritzker family wealth across branches is estimated at $30–35 billion.

The Pritzkers are also actively expanding into advising other family offices — TPO recently invested in Wellspring Family Office, a multi-family office managing $4.2 billion for 75 families, with TPO's described investment horizon of 50 to 70 years. This is the co-investing and platform model Christina describes: using the family office's track record and permanent capital to partner with other families, building revenue and scale beyond the original family's balance sheet.

The Global Picture as of April 2026

To put these examples in context:

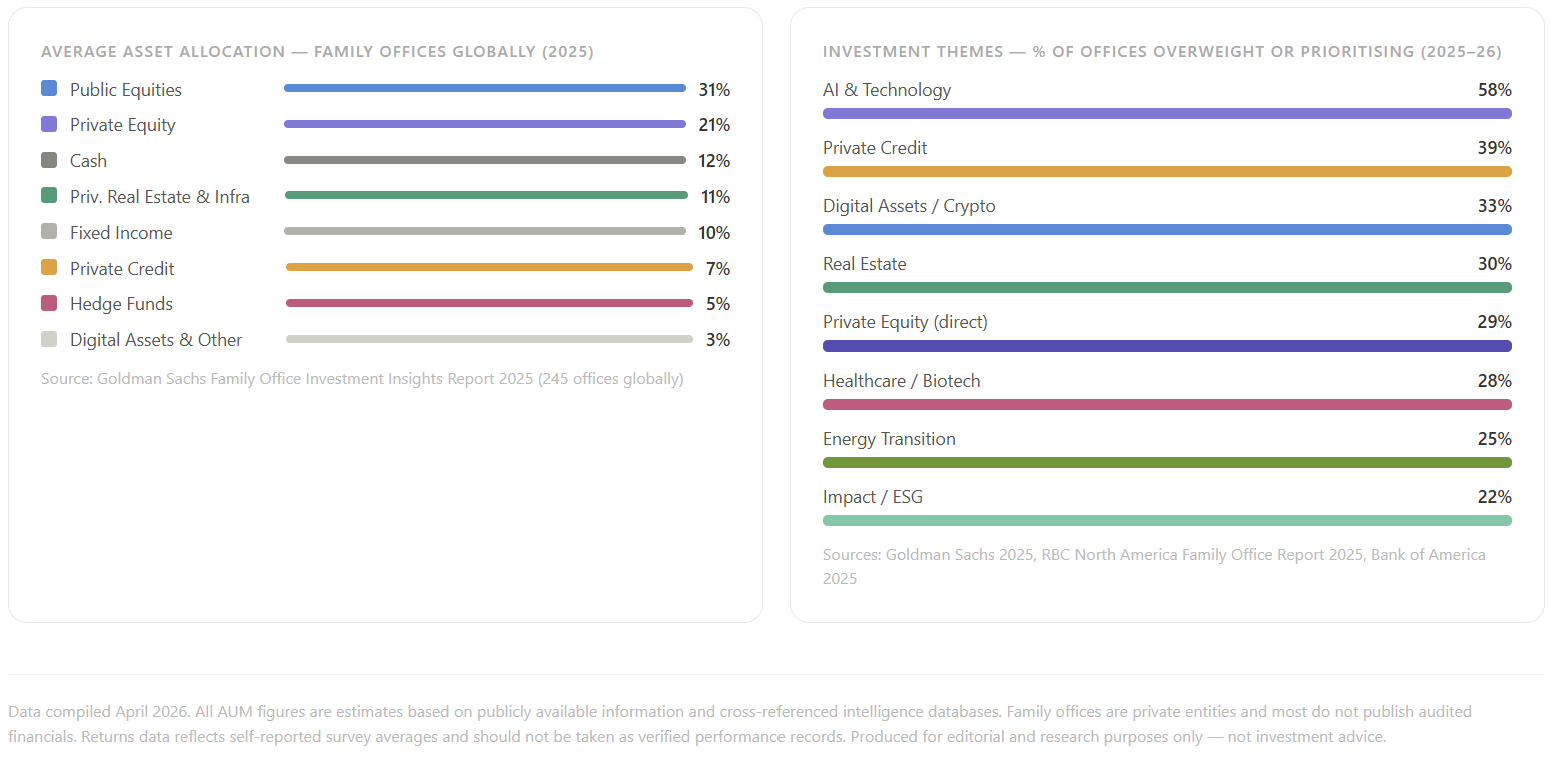

- Total global family office AUM is estimated at $5–10 trillion

- The global count of significant family offices now exceeds 8,000, up from approximately 1,285 in 2019

- The average family office manages around $2 billion in assets with a team of roughly 12 people

- The US hosts the world's highest concentration, accounting for the largest single share of the global total

- 69% of family office deals are made alongside other family offices — co-investing is the dominant deal structure

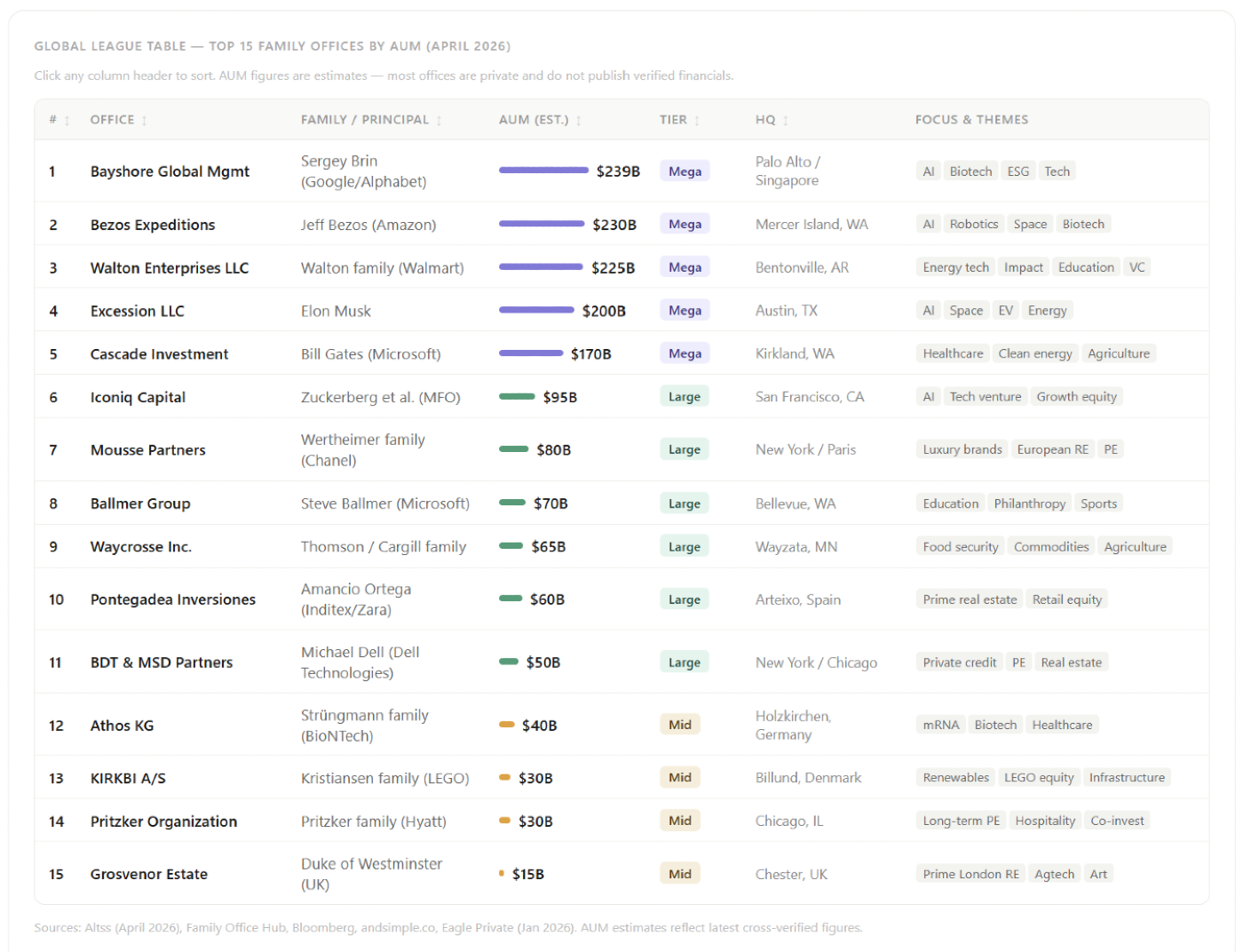

- The top 10 family offices globally each control $50–200 billion+ in assets

The largest family offices in the world as of 2026 include Walton Enterprises (Walmart), Cascade Investment (Bill Gates), Bezos Expeditions, Hillspire (Eric Schmidt), and Iconiq Capital (linked to Mark Zuckerberg), managing estimated AUM of $50–200+ billion each. MSD/BDT at $50 billion sits comfortably in the top tier.

Is the Family Office an American Concept? The British and European Noble Model

The answer is no — and the history here reframes the entire conversation in a meaningful way.

The term "family office" in its modern form is often traced to the United States, typically attributed to the Rockefeller family office established around 1882. But the concept — a dedicated professional structure to manage dynastic wealth, land, staff, philanthropy, art collections, and generational succession — is centuries older and deeply European, specifically British, in origin.

What the British landed gentry ran for centuries were called estate offices — managed by agents, stewards, and bursars who handled tenancy contracts, agricultural yields, legal title, household accounts, charitable giving, and succession planning. This is, structurally, a family office. It simply did not carry that name.

The oldest and most striking living example is the Grosvenor Estate, the family office of the Duke of Westminster. Its history begins in 1677, when 12-year-old heiress Mary Davies married Sir Thomas Grosvenor and brought with her 500 acres of land north of the Thames. The family developed what is now Mayfair in the 1720s and Belgravia from the 1820s onward. Today the Grosvenor Estate manages approximately £11.8 billion (roughly $15 billion) in assets across 62 international cities, with offices in 14 countries, structured across four divisions: Britain and Ireland, the Americas, Europe, and Asia Pacific. It also maintains a dedicated philanthropic foundation, a fine art collection, and historic archives — all managed by distinct teams under a formal Family Office Board with clearly separated roles.

Sound familiar? That is Christina Wing's three-function model — investment, administration, philanthropy — built across 350 years of continuous operation, predating the United States by a century.

The key structural difference between the British/European noble model and the American family office model is the origin asset:

The British and European model is built around land and property — held for centuries, generating rental income, appreciating through urban development, managed as a stewardship obligation across generations. You do not "exit" Mayfair. You manage it for the next duke.

The American model is more typically built around a liquidity event — a technology company sold, a business taken public, a founder cashing out — and the family office is constructed to deploy that liquid capital intelligently going forward. The European model is about stewarding what exists. The American model is more often about putting new capital to work.

And yet: both are converging. London has become a global hub for both ancient-estate family offices and new-money single-family offices from across the world. The UK's top family offices in 2025–2026 include the Grosvenor Estate alongside Weybourne Group (the Dyson family office), Reuben Brothers, Hinduja Family Office, and Alta Advisers (managing $20 billion for the Rausing family). The continent has its own long tradition — the Rothschilds maintained structured family investment offices across Europe from the early nineteenth century, arguably the most sophisticated cross-border family financial architecture ever built.

What America added to this centuries-old concept was the investment-management emphasis, the formal industry infrastructure, the compensation benchmarks, and — crucially — the language of business governance applied to what had previously been managed as a matter of aristocratic tradition. Christina Wing's insight that family offices need to be treated as businesses is, seen through this lens, less a new idea than a translation: taking what the Grosvenors have known implicitly for three and a half centuries and making it legible for a new generation of founders who came to wealth through disruption rather than inheritance.

Resources

On the conversation that inspired this post:

- Christina Wing — Harvard Business School faculty profile: hbs.edu

- Wingspan (Christina Wing's private advisory practice): search "Wingspan Christina Wing"

- YouTube interview: "Why 90% of Family Offices Fail — Harvard's Christina Wing Explains" — the source conversation for this post

On family office structure and the industry:

- The State of Family Offices 2026 — Mr Family Office: mrfamilyoffice.com

- The 50 Largest Family Offices in the World (2026) — Altss: altss.com

- Family Offices in the United States: The Complete Guide 2026 — Family Office Hub: familyofficehub.io

- Top 10 Largest Family Offices in the UK & Ireland (2025) — Altss: altss.com

- BlackRock Global Family Office Report 2025: blackrock.com

- UBS Global Family Office Report 2025: ubs.com

- KPMG Agreus Global Family Office Compensation Benchmark Report 2025: kpmg.com

On the specific family offices referenced:

- 1888 Investments (Koch Family Office) — Altss profile: altss.com

- DFO Management (formerly MSD Capital, Dell family) — Wikipedia: en.wikipedia.org/wiki/DFO_Management

- BDT & MSD Partners analysis (2025): theesk.org

- The Pritzker Organization: pritzkerorg.com

- Pritzker Group: pritzkergroup.com

On the British and European noble wealth management tradition:

- Grosvenor Estate (Duke of Westminster family office): grosvenorestate.com

- Grosvenor Group — Wikipedia: en.wikipedia.org/wiki/Grosvenor_Group

- Landed Gentry — Wikipedia (historical context): en.wikipedia.org/wiki/Landed_gentry

- Family Office Hub — UK Single Family Offices: familyofficehub.io

On family governance, generational dynamics, and the rising generation:

- University of Chicago Booth School of Business — Family Office Initiative: chicagobooth.edu/research/family-office-initiative

- Extreme Ownership by Jocko Willink and Leif Babin (referenced in the Christina Wing conversation)

![Obsidian Essay | Leadership] A Summer Breeze, a Rooftop, and the Life of a Habsburg Daughter - Maria Carolina of Austria](https://storage.ghost.io/c/2a/9e/2a9e2b04-30f6-4166-8010-a3730d2eb719/content/images/size/w720/2026/07/Maria-Carolina-1.png)

![Leadership] Ivanka Trump on Building an Authentic Life](https://storage.ghost.io/c/2a/9e/2a9e2b04-30f6-4166-8010-a3730d2eb719/content/images/size/w720/2026/06/26-06-06-12-37-18-997_deco.png)

![Cartier Dialogues | Leadership] Strength Reimagined: Leadership, Kindness and the Courage to Defy Expectations](https://storage.ghost.io/c/2a/9e/2a9e2b04-30f6-4166-8010-a3730d2eb719/content/images/size/w720/2026/06/Screenshot-2026-06-16-064930-1.png)

Comments ()